|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| �

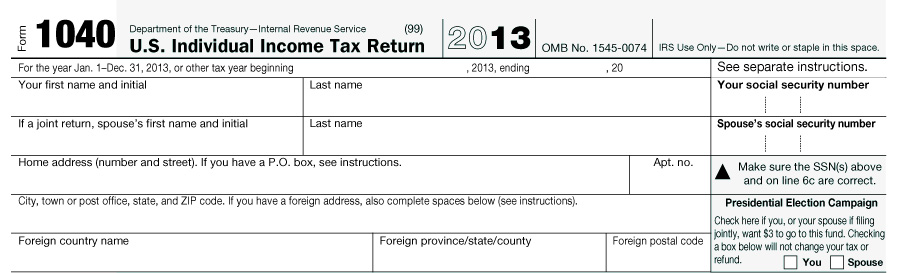

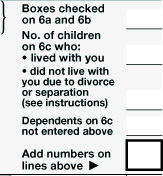

Interactive Tax Forms

The Tax Policy Center has put together this interactive tool to tell you a little about what is behind the tax forms. What does each line mean? How many people make an entry? How does it affect revenues and the distribution of tax burdens across income categories? This inaugural version includes form 1040�the most commonly used return�along with Schedule A for itemized deductions. Over time, we will update information and add more forms. Click on a link to bring up a form. Then hover your cursor over a line to see basic information and click to bring up a box with additional information.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||